You are currently viewing SemiWiki as a guest which gives you limited access to the site. To view blog comments and experience other SemiWiki features you must be a registered member. Registration is fast, simple, and absolutely free so please, join our community today!

Could Intel's 14A be delayed due to 18A’s poor customer traction, no major new foundry clients announced at Intel Foundry Direct Connect 2025, financial losses, and bureaucratic hurdles? TSMC’s lead and Intel’s cautious High-NA EUV approach further slowing progress, pushing competitive foundry ambitions to 2027, or beyond.

Intel covered this at the event last month. For me, Intel 18A is a proof point for the foundry business. If Intel wants to be in the foundry business 14a cannot be delayed. It needs to be on par with the TSMC 16A timeline but hopefully with better PPA. I would not bet on the first foundry version of 14A having HNA-EUV, delivering 14A on time is much more important if Intel Foundry wants to catch a whale, absolutely.

Intel covered this at the event last month. For me, Intel 18A is a proof point for the foundry business. If Intel wants to be in the foundry business 14a cannot be delayed. It needs to be on par with the TSMC 16A timeline but hopefully with better PPA. I would not bet on the first foundry version of 14A having HNA-EUV, delivering 14A on time is much more important if Intel Foundry wants to catch a whale, absolutely.

Intel covered this at the event last month. For me, Intel 18A is a proof point for the foundry business. If Intel wants to be in the foundry business 14a cannot be delayed. It needs to be on par with the TSMC 16A timeline but hopefully with better PPA. I would not bet on the first foundry version of 14A having HNA-EUV, delivering 14A on time is much more important if Intel Foundry wants to catch a whale, absolutely.

It is more real to count the effective capacity (considering fab and probe or FT yield). Is the IFS capacity built for 18A and 14A available in public?

Could Intel's 14A be delayed due to 18A’s poor customer traction, no major new foundry clients announced at Intel Foundry Direct Connect 2025, financial losses, and bureaucratic hurdles? TSMC’s lead and Intel’s cautious High-NA EUV approach further slowing progress, pushing competitive foundry ambitions to 2027, or beyond.

First floated in 2021, the 2nm-class node was meant for top-shelf CPUs and GPUs, but with delays to its follow-up 14A node, Intel is now rejigging 18A to cover more ground.

Chipzilla’s CEO Lip-Bu Tan leans into realism Troubled Chipzilla is stretching its long-promised 18A process into two new variants aimed at feeding the AI beast and mainstream punters. First floated in 2021, the 2nm-class node was meant for top-shelf CPUs and GPUs, but with delays to its...

Ultimately it comes down to the economics of the node.

If 18A doesn’t have enough volume to pay off the capex in 3-5 years, then the only way to make the numbers work is to try and drag out the life of the node. But then the next node is delayed and Intel will have an even bigger problem at 14A.

Ultimately it comes down to the economics of the node.

If 18A doesn’t have enough volume to pay off the capex in 3-5 years, then the only way to make the numbers work is to try and drag out the life of the node. But then the next node is delayed and Intel will have an even bigger problem at 14A.

My opinion is that the pace of shrink dropping is extremely negative for leading edge fabs, including TSMC.

It means the performance gap between leading edge and trailing edge will shrink over time, and that will provide an opening for the Chinese fabs to catch up. They will not be blocked on EUV forever.

My opinion is that the pace of shrink dropping is extremely negative for leading edge fabs, including TSMC.

It means the performance gap between leading edge and trailing edge will shrink over time, and that will provide an opening for the Chinese fabs to catch up. They will not be blocked on EUV forever.

Ultimately it comes down to the economics of the node.

If 18A doesn’t have enough volume to pay off the capex in 3-5 years, then the only way to make the numbers work is to try and drag out the life of the node. But then the next node is delayed and Intel will have an even bigger problem at 14A.

In January 2023 Intel changed its equipment depreciation from 5 years to 8 years (TSMC sticks to the 5-year depreciation schedule) in order to make Intel's financial statements look better.

It may cosmetically make Intel's cost lower than it should be for the first five years but cause higher cost for the year 6 through year 8 in competing against other foundries.

With this kind of financial manipulation Intel is still struggling to make itself profitable.

First floated in 2021, the 2nm-class node was meant for top-shelf CPUs and GPUs, but with delays to its follow-up 14A node, Intel is now rejigging 18A to cover more ground.

Chipzilla’s CEO Lip-Bu Tan leans into realism Troubled Chipzilla is stretching its long-promised 18A process into two new variants aimed at feeding the AI beast and mainstream punters. First floated in 2021, the 2nm-class node was meant for top-shelf CPUs and GPUs, but with delays to its...

Intel foundry needs real external customers who have real volume and are really happy on 18A to continue. While it might be nice to say "18A is proof of concept and the next nodes will have sales and grow" you cannot build it and spend it and still have no one come for 18A (the great inflection point). It is financially unacceptable.

Intel foundry needs real external customers who have real volume and are really happy on 18A to continue. While it might be nice to say "18A is proof of concept and the next nodes will have sales and grow" you cannot build it and spend it and still have no one come for 18A (the great inflection point). It is financially unacceptable.

This is why Intel must stay together. Intel products can fill the fabs (if they use Intel instead of TSMC) while Intel Foundry gets additional customers. It is a hand-in-hand thing. If Intel is doing $50-60B in product revenue and additional $5-10B in foundry revenue (by 2030) would be helpful in filling the fabs and coffers, right?

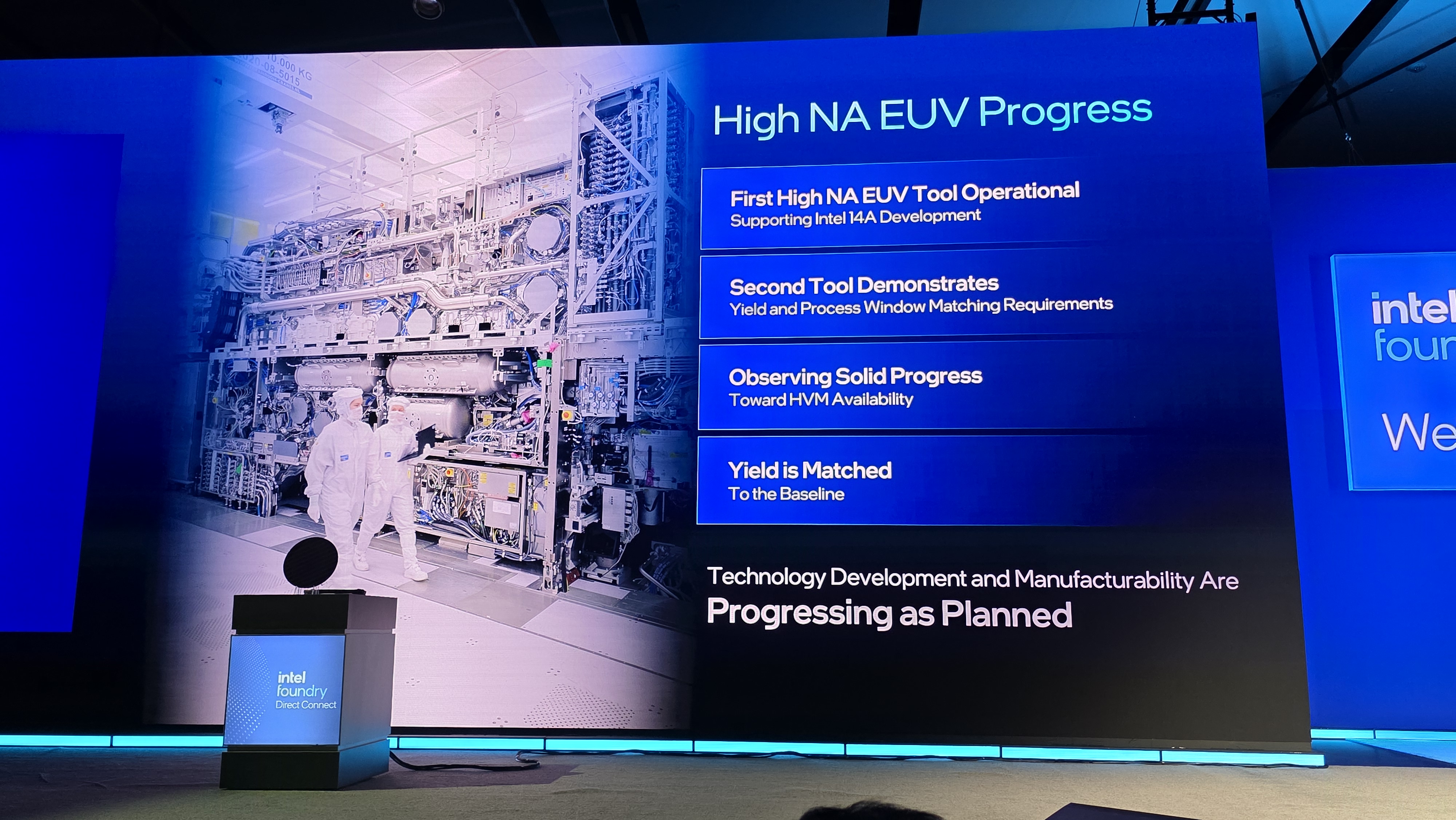

"Intel will only use High-NA EUV on a small number of layers of the 14A node (the exact number isn’t known), while other machines of varying resolutions will be used for the other layers."

Intel foundry needs real external customers who have real volume and are really happy on 18A to continue. While it might be nice to say "18A is proof of concept and the next nodes will have sales and grow" you cannot build it and spend it and still have no one come for 18A (the great inflection point). It is financially unacceptable.

Exactly. It takes tens of billions to develop a new node, and it's increasing exponentially over time. Your strategy can't be "I'm going to spend $20b on a proof of concept at 18A, and hopefully that will lead to sales on 14A, which will cost $30b to develop" unless the goal is to go bankrupt.

Exactly. It takes tens of billions to develop a new node, and it's increasing exponentially over time. Your strategy can't be "I'm going to spend $20b on a proof of concept at 18A, and hopefully that will lead to sales on 14A, which will cost $30b to develop" unless the goal is to go bankrupt.

How much of Intel Foundry business will be internal at the break even point? 75%? And what wafer price will the Intel Design groups be paying? Certainly not cost like Samsung Foundry.